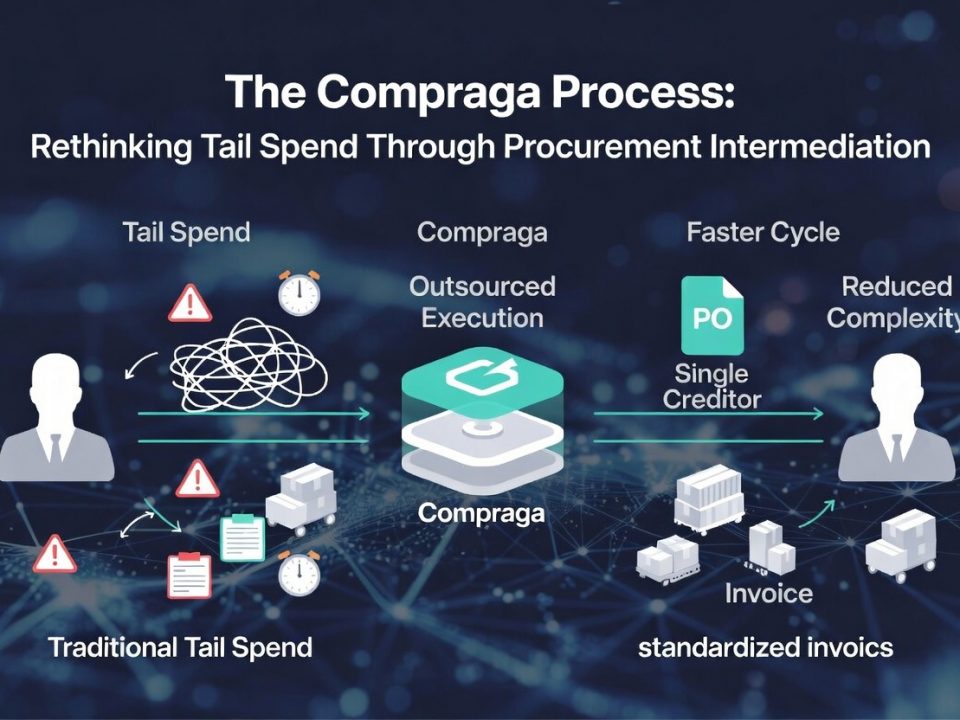

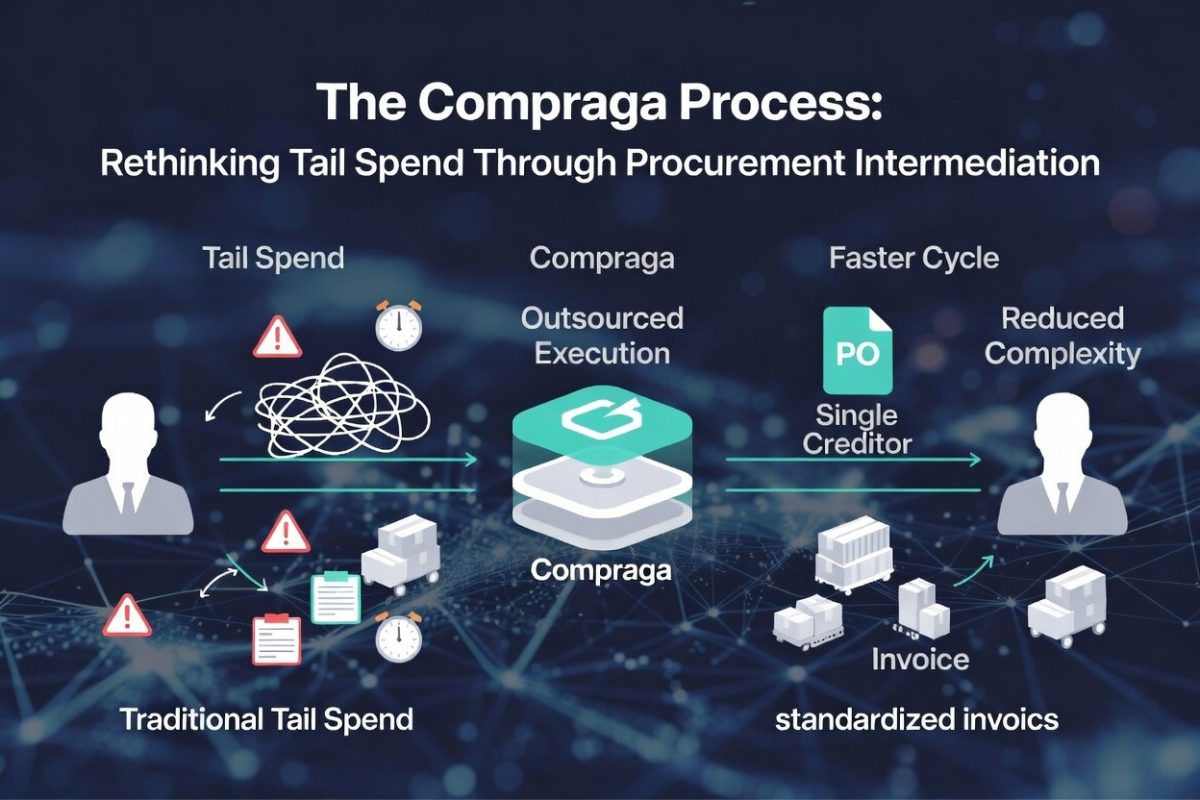

The Compraga Process

März 10, 2026

Purchase Request to Payment

Mai 3, 2026

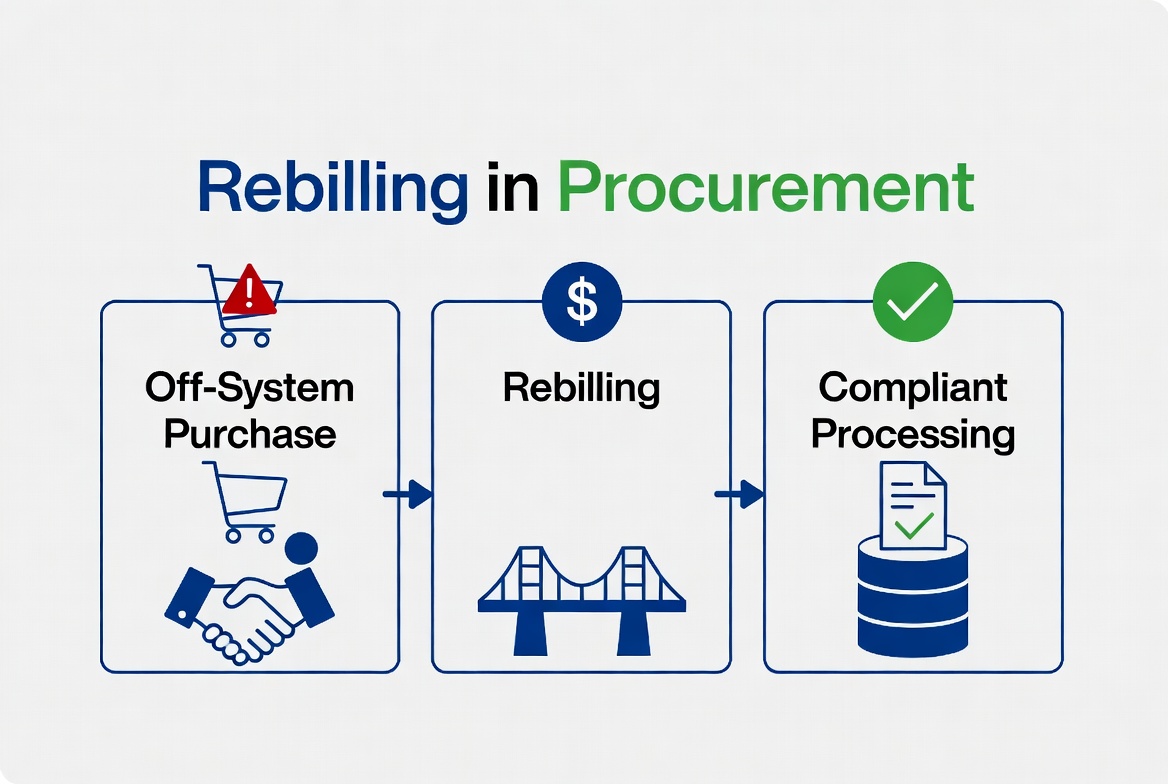

Rebilling in Procurement: How to Handle Off-System Purchases Without Breaking Finance

In a well-structured procurement environment, every supplier is onboarded, every purchase flows through defined systems, and every invoice matches an approved order. That is the theory. In practice, companies regularly encounter situations where this structure breaks down. Urgent purchases are made outside the system, niche suppliers are engaged without proper onboarding, and internal teams prioritize speed over process. When the invoice arrives, finance is left with a problem that cannot be processed through standard workflows. This is where rebilling enters the picture.

Rebilling is not a strategy; it is a workaround. It typically occurs when a third party steps in to formalize a transaction that has already taken place informally. Instead of paying the original supplier directly, the company pays an intermediary who has purchased the goods or services on its behalf and then re-invoices them in a compliant format. This allows the transaction to be recorded within the system, but it also introduces a layer of complexity that carries financial, legal, and operational implications.

The underlying issue is not the invoice itself, but the breakdown of procurement discipline that led to it. When a supplier is not properly onboarded, key elements are missing. There may be no verified tax information, no contractual framework, and no alignment with internal compliance standards. Processing an invoice under these conditions exposes the company to risk. Finance teams are forced to make exceptions, override controls, or delay payments while attempting to reconstruct the transaction. Each of these options has a cost, whether in time, accuracy, or exposure.

Rebilling provides a way to restore structure after the fact. The intermediary assumes the role of the supplier, issuing an invoice that meets the company’s requirements. This can include proper tax documentation, standardized formatting, and alignment with internal approval processes. From an operational perspective, this simplifies processing. The invoice can be matched, approved, and paid without requiring changes to existing systems. The immediate problem is resolved, and the transaction is brought back into the formal framework.

However, this apparent simplicity masks a more complex set of dynamics. The introduction of an intermediary changes the nature of the transaction. The original supplier relationship is replaced, at least on paper, by a new contractual flow. This raises questions about liability, ownership, and accountability. If there are issues with the goods or services, it may not be immediately clear who is responsible. The intermediary may not have the same level of control or knowledge as the original supplier, which can complicate dispute resolution.

Tax treatment is another critical area. Rebilling must be structured carefully to ensure compliance with VAT and other regulatory requirements. The intermediary is not merely passing through costs; it is engaging in a commercial transaction. This means that VAT must be applied correctly, and the nature of the service or goods must be accurately reflected. Errors in this process can lead to incorrect tax filings, penalties, or challenges during audits. The probability of such issues is not negligible, particularly in cross-border transactions where tax rules are more complex.

From a financial perspective, rebilling introduces additional cost. The intermediary typically applies a margin to cover its role in the transaction. This may be explicit or embedded in the pricing, but it represents a real increase in procurement cost. While this may be justified in situations where rebilling prevents larger disruptions, it is not a sustainable solution at scale. If a significant portion of procurement activity relies on rebilling, the cumulative impact on margins can be material.

The frequency of rebilling is often an indicator of deeper structural issues within procurement. When off-system purchases occur regularly, it suggests that existing processes are either too rigid or not aligned with operational needs. Employees bypass procurement because it slows them down or does not accommodate the types of purchases they need to make. In this context, rebilling becomes a recurring mechanism rather than an exception. The probability of this pattern emerging in organizations with decentralized procurement and high tail spend can exceed 50 percent.

Risk exposure increases as rebilling becomes more common. Each transaction carries potential gaps in documentation, unclear audit trails, and misalignment between the actual flow of goods and the recorded flow of invoices. During an audit, these discrepancies can raise questions about the integrity of procurement processes. The likelihood of audit findings related to such issues can rise significantly, particularly in environments with strict compliance requirements. In some cases, the presence of frequent rebilling may be interpreted as a systemic control failure rather than isolated exceptions.

In more challenging scenarios, the weaknesses associated with rebilling are amplified. Under increased regulatory scrutiny, for example, authorities may examine the substance of transactions more closely. If the intermediary is seen as a pass-through without real economic activity, the structure may be challenged. This can lead to reclassification of transactions, tax adjustments, and potential penalties. The probability of such outcomes depends on the quality of the rebilling structure, but it can increase by 15 to 25 percentage points in high-scrutiny environments.

Liquidity pressure introduces another layer of complexity. Intermediaries involved in rebilling often take on short-term financial exposure, paying suppliers before receiving payment from the client. In stable conditions, this can be managed through standard payment terms. In a tightening credit environment, however, this model becomes more fragile. If intermediaries face constraints, they may require faster payment or higher margins, increasing cost and reducing flexibility for the company. This shifts part of the working capital burden back onto the organization, undermining one of the perceived benefits of rebilling.

Despite these challenges, rebilling has a legitimate role when used selectively and structured correctly. It can serve as a bridge between operational reality and financial control, allowing companies to handle exceptions without disrupting their systems. The key is to ensure that it remains an exception. This requires addressing the root causes of off-system purchasing. Procurement processes must be flexible enough to accommodate urgent and non-standard needs, while still maintaining control and visibility. Supplier onboarding must be efficient, reducing the incentive to bypass it. At the same time, clear guidelines must be established for when and how rebilling can be used, including defined responsibilities, documentation requirements, and approval processes.

{kind=link}

{kind=link}